|

| Source: https://www.youtube.com/watch?v=1UQXfnp8YlM |

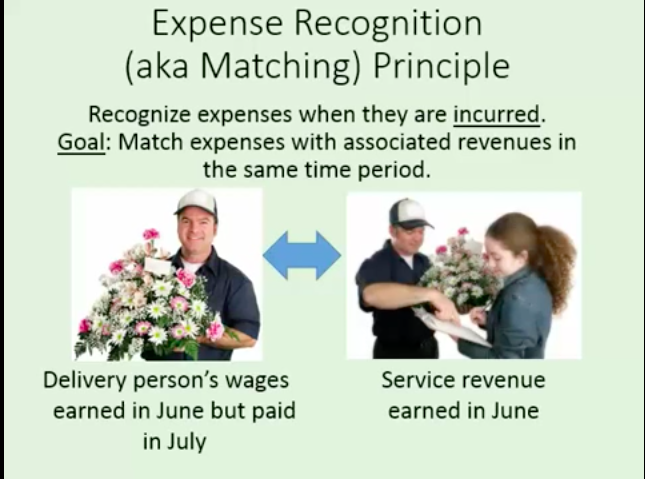

The expense principle states that whatever expenses that

occur in a single period should be recorded alongside whichever revenue to

which they match up with. For example, let’s say a company pays $100,000 for

their merchandise, which the company sells the following month for $150,000,

with the expense recognition principle, the $100,000 would not be acknowledged

until the following month, alongside its related revenue of $150,000.

Things like income taxes, can be effected by this expense

principle. An income tax is a tax set in place by the government, so they receive

a set, specific amount from a person, or company’s yearly income. To relate

this back to the earlier example, the company’s income tax in the first month would

be underpaid since the expenses were higher than revenue (because they paid

$100,000 but did not have any recorded revenue with it), and the following

month would be overpaid when the expenses were low and revenue was higher.

|

| Source: https://en.wikipedia.org/wiki/Income_tax |

By Katie Howard

Citations:

No comments:

Post a Comment